Ssae 18 Control Objectives List

The Astounding Ssae 16 Audit Soc 1 Soc 2 Soc 3 From Lazarus Alliance With Regard To Ssae 16 Report In 2020 Best Templates Professional Templates Business Template

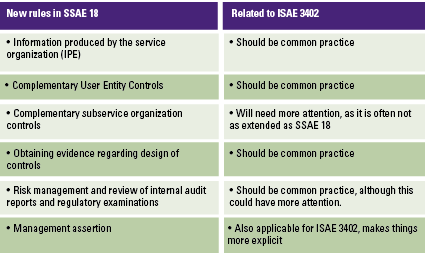

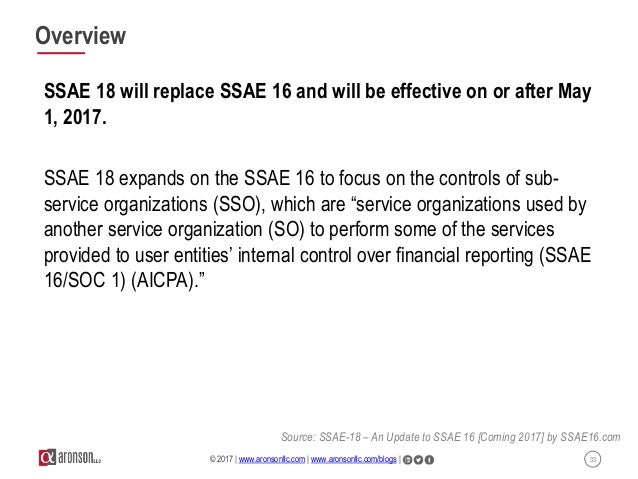

The New Us Assurance Standard Ssae 18 Compact

The Clarity Project Ssae 18 Essentials

Https Guidehouse Com Media Www Pdfs Legacy Guidehouse Whitepapers What Are Ssae No 18s And How Pdf

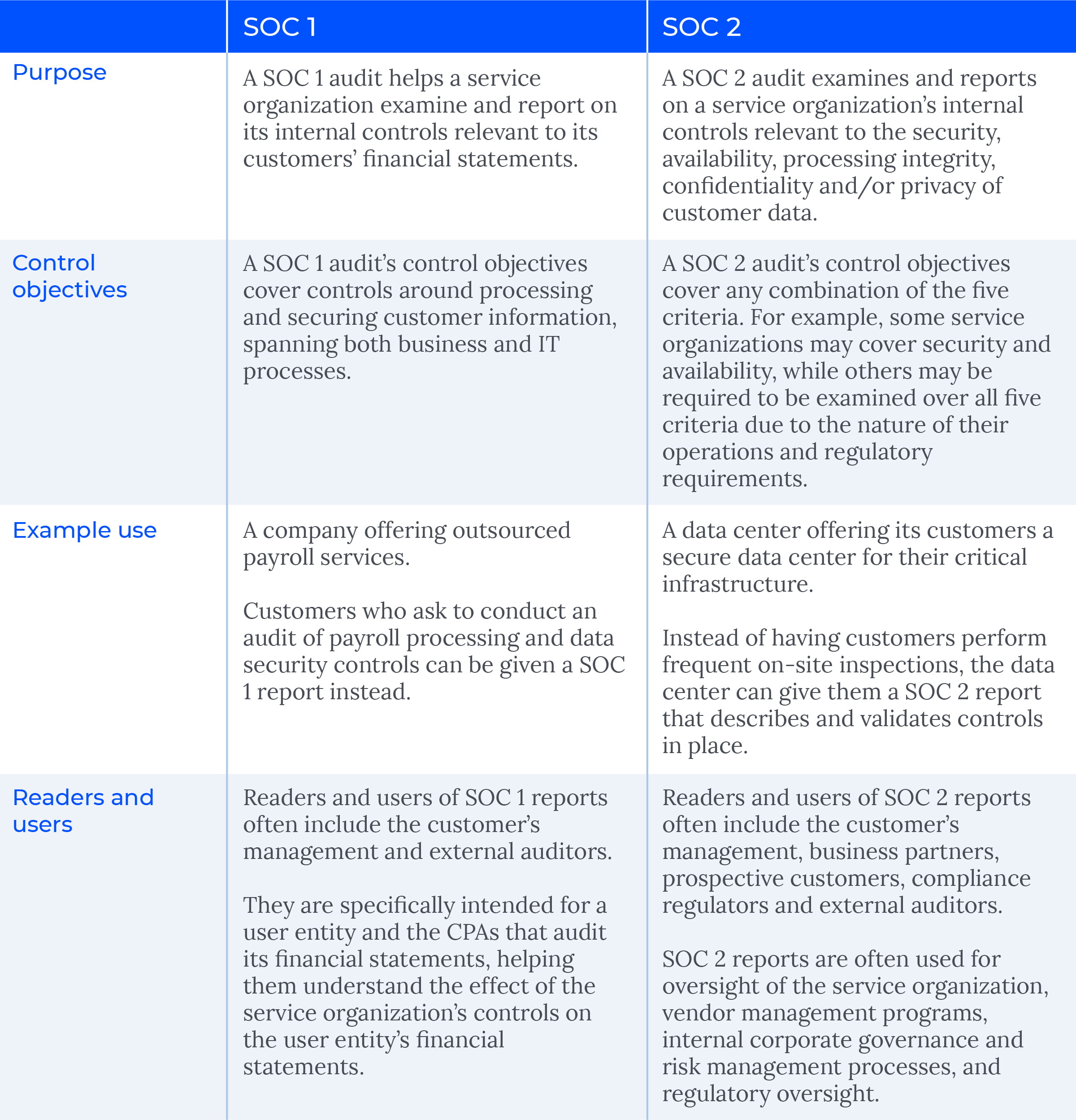

Soc 1 Vs Soc 2 What S The Difference Wipfli

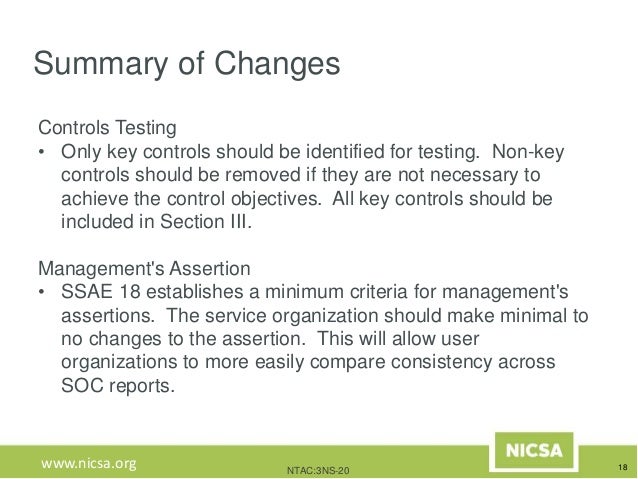

Preparing For A Soc Audit A Checklist

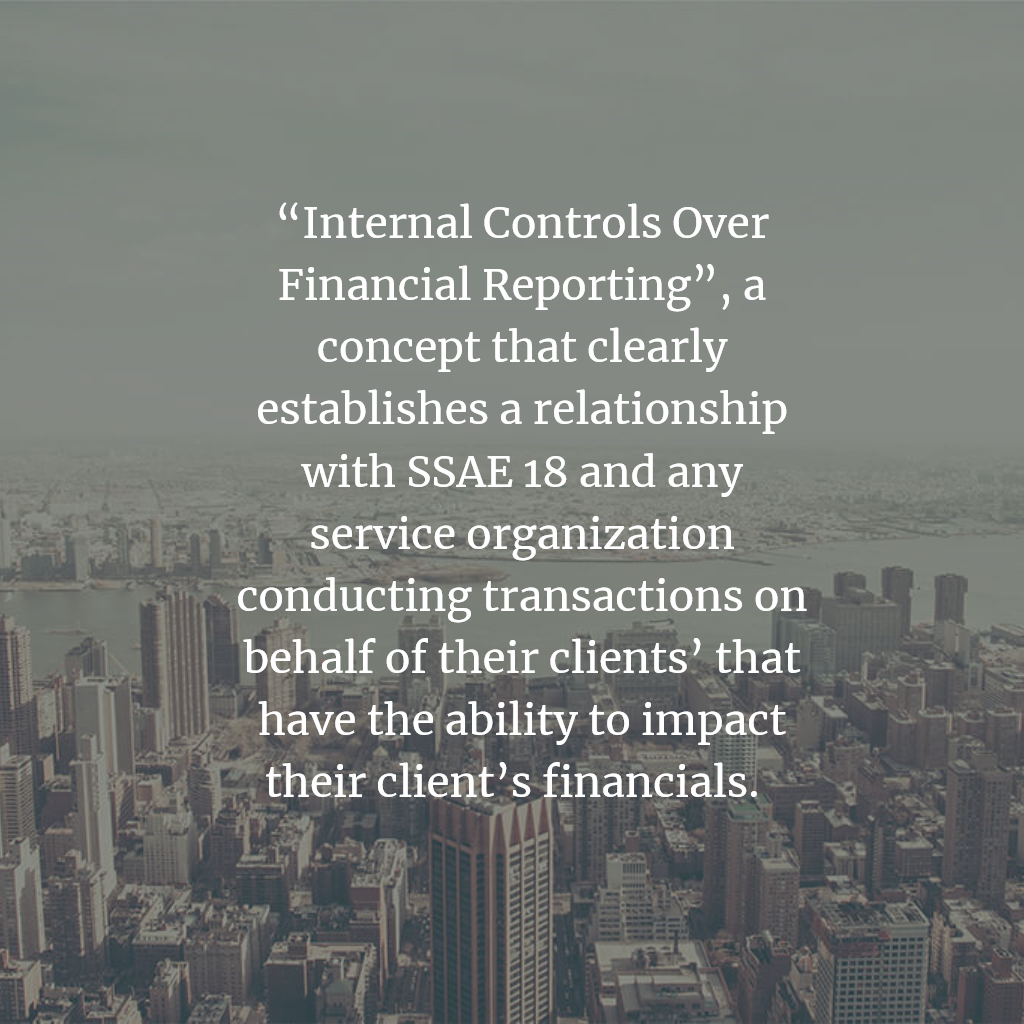

A clearer view of attestation standards for service organizations 1.

Ssae 18 control objectives list.

Ssae 18 Soc Audit And Attestation Services Riskpro India Connect With Risk Professionals

Business Trip Report Template Pdf 3 In 2020 Report Writing Template Sales Report Template Report Writing

Ssae 18 Soc 2 Certified Lifeline Data Centers

Control Objectives Activities What Are They What S Appropriate

Soc 1 Ssae 18 Audit Checklist For Auditing Success For Denver Co Businesses Ndb Accountants

Introduction To Ssae 18 And Service Organization Controls Soc Examinations Mckonly Asbury

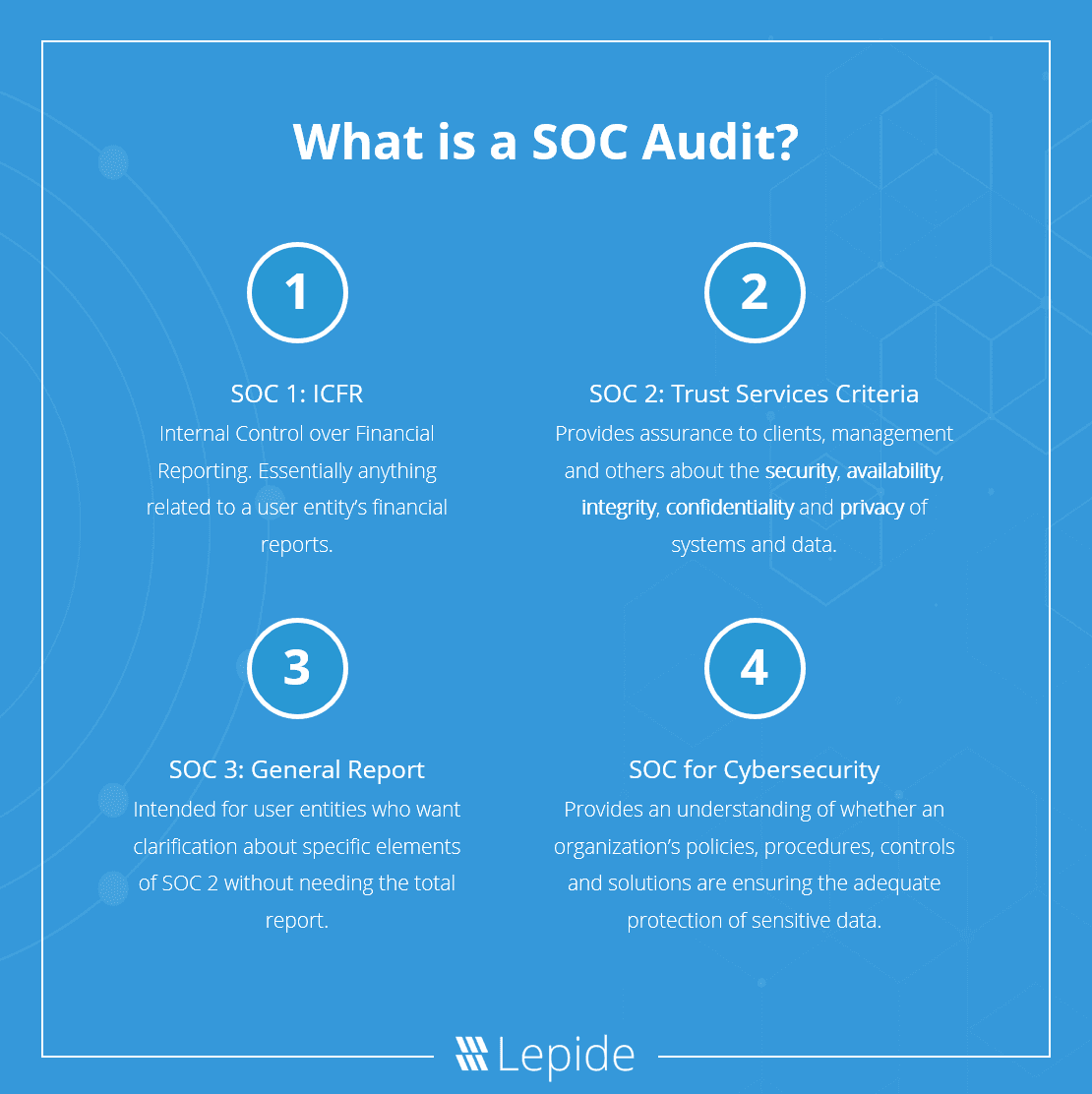

Soc For Service Organizations Information For Cpas

Ssae 18 The Full Overview For Vendor Management

Webinar Soc Reports 101 Boost Your Business Bottom Line

Soc And Ssae Reporting Services Coalfire

Https Www Giac Org Paper Gsna 553 Understanding Service Organizations Ssae 111066

What Is Soc 1 Ssae 18 Introduction And Overview

Soc 1 Type 2 Compliance Audit Ssae 18 Vs Soc 1 Faq Isae 3402 Icfr Sox Auditor

Health And Safety Incident Report Form Template 9 Templates Example Templates Example In 2020 Health And Safety Incident Report Report Template

What Is A Soc 1 Report Soc 1 Videos Kirkpatrickprice

2020 Trust Services Criteria Principles For Soc 2 Tsp Section 100

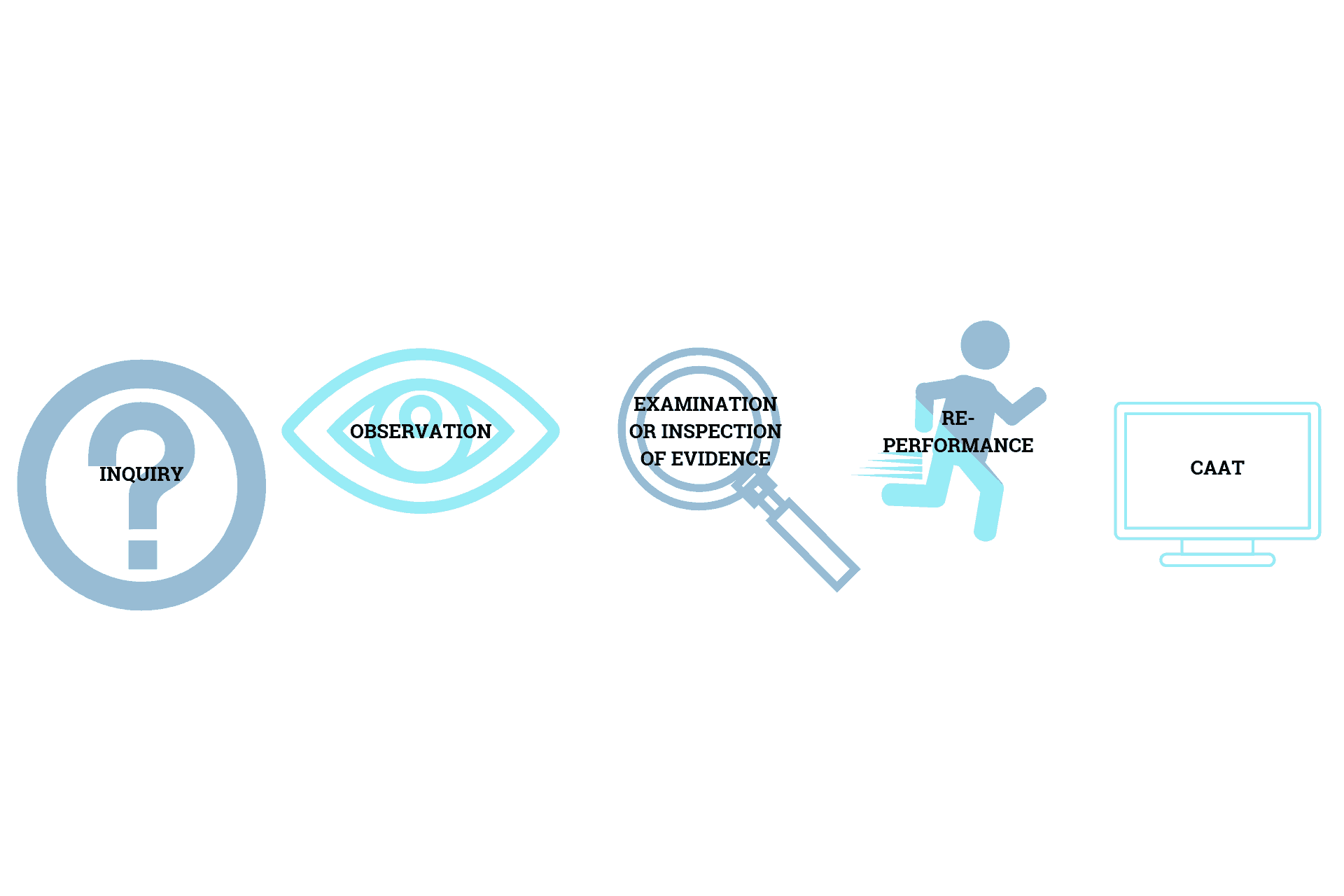

5 Types Of Testing Methods Used During Audit Procedures I S Partners

Https Www Dcma Mil Portals 31 Documents Policy Dcma Man 4301 11v2 Pdf Ver 2019 10 02 110921 410

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsickyqjeazia57ci0f4m Y6y7cnzyszorcrmv La07y93xw13k Usqp Cau

Soc 1 Vs Soc 2 Reports Difference Between Determining Needs

Wk6gzehrjrdgm

Subservice Organizations Carve Out Audit Vs Inclusive Audit Methods

Soc 2 Compliance Audit Checklist 2020 Know Before Audit

What Is A Soc 1 Report When Is It Required Who Needs It

Source : pinterest.com